Publié le 15/04/19

Let investors’ growing appetite for sustainable finance benefit culture

Paper* proposed and written by Pascale Thumerelle, Founder of Respethica

Investors are more and more aware of their vital role in promoting sustainable development by practicing sustainable finance. They have to meet the growing expectations of institutions, business sector and civil society to build responsible economies that take environment, social and societal impact into consideration. They also ensure that they will avoid the crisis that happened ten years ago. Their commitment is crucial to support companies that are determined to create value not only for themselves but also for all their stakeholders defined as people « impacted by the decisions taken by companies ».[1]

From Sustainable Development to Sustainable Investing

The concept of sustainable development, originated in the 1970s was given a spotlight in the « Our Common Future » report published in 1987 by the World Commission of Environment and Development (WCED). This Comission chaired by Gro Harlem Brundtland (the first woman to have ruled Norway as a Prime Minister) issued a statement and gave a definition. The statement was : to build a long term development, economic growth, social cohesion and environmental protection must go hand in hand. The definition proposed by this report was « Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. » The intergenerational dimension stresses the need to consider solidarity and responsibility towards our children and following generations. It means companies and investors have to anticipate the outcomes of their decisions over time.

In its conclusion, the 1987 Brundtland report required a global strategy that « aims to promote harmony among human beings and between humanity and nature ». The 2030 Agenda for sustainable development adopted in September 2015 by the heads of states and governments at the UN Sustainable Development Summit, « aims to transform our world and to improve people’s lives and prosperity on a healthy planet. It applies to all countries through partnerships and peace. Countries, regions, cities, the business sector and civil society are actively engaged in implementing the Agenda and the Sustainable Development Goals. » [2] This great and noble ambition has to be shared by the international community called upon to act responsibly.

To be promoted loud and clear, the credo is fueled by the 17 Sustainable Development Goals (SDGs) to be achieved by 2030 and based on the three pillars of sustainability : social, environmental and economic. The UN SDGs focus on five priorities (P) : planet, people, prosperity, peace and partnership.

More and more investors use these SDGs to align their practices according to their commitment to a more responsible finance system.

The former UN General Secretary Kofi Annan had very well understood the need to « plant the seeds for modern corporate and financial sustainability ». He played a critical role to bring governments, companies and investor industry together to help address many of the world’s challenges. First Kofi Annan mobilised the private sector through the Global Compact’s launch in 2000 : “We, the United Nations, initiate a Global Compact of shared values and principles, which will give a human face to the global market”. With fewer than 50 signatory businesses, the Global Compact now brings together more 12,000 corporate signatories from 160 countries. Then Kofi Annan turned to investors so that « the owners of those companies and the custodians of savers’ financial futures might explore the role they could play in building a more sustainable future for the benefit of those they serve. [3] » The PRI were launched in April 2006 at the New York Stock Exchange. Since then the number of signatories has grown from 100 to over 2,300 in 2018. These Principles developed by investors for investors reflect the integration of environmental, social and governance (ESG) issues to their investment practices.

In search of fundamental solutions for building more inclusive societies, sustainable investing has grown at a rapid pace in the last decade.

The letter sent last year by the Blackrock’s Chairman and CEO Larry Fink to all CEOs testifies to this development. The world’s largest asset manager CEO clearly stated : « […] Society is demanding that companies, both public and private, serve a social purpose. To prosper over time, every company must not only deliver financial performance, but also show how it makes a positive contribution to society. Companies must benefit all of their stakeholders, including shareholders, employees, customers, and the communities in which they operate. Without a sense of purpose, no company, either public or private, can achieve its full potential. It will ultimately lose the license to operate from key stakeholders. It will succumb to short-term pressures to distribute earnings, and, in the process, sacrifice investments in employee development, innovation, and capital expenditures that are necessary for long-term growth. […] »[4]

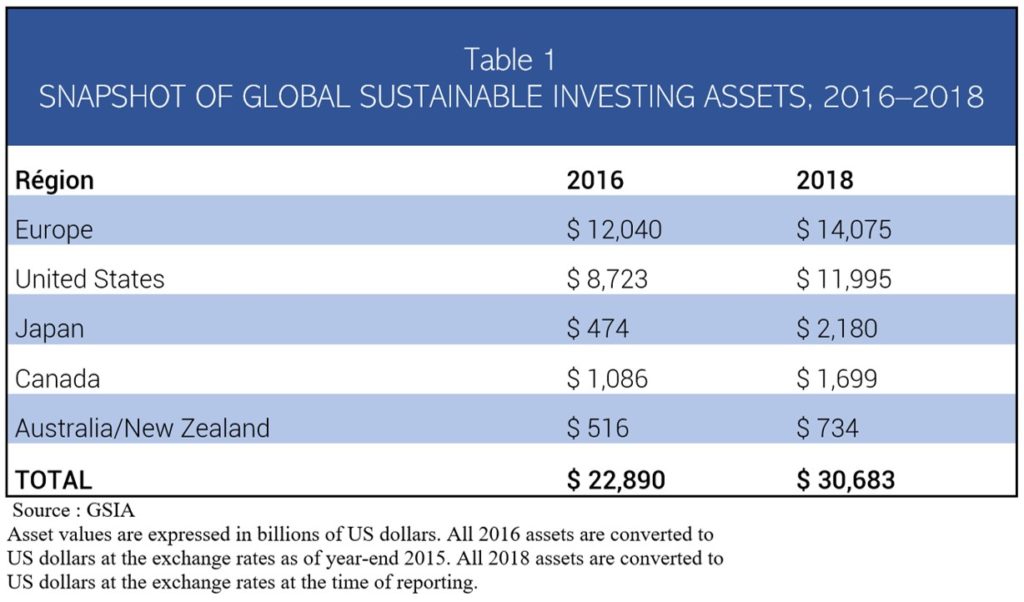

The Global Sustainable Investment Alliance (GSIA) defines sustainable investing as « an investment approach that considers environmental, social and governance (ESG) factors in portfolio selection and management » [5]. It represents an increasingly important part of overall investment. According to GSIA 2018 Global Sustainable Investment Review « at the start of 2018, global sustainable investment reached $30.7 trillion in the five major markets shown in Table 1 (below), a 34 percent increase in two years ».

According to diverse sources, global assets under management reached between $80 and $85 trillion. If we compare these two figures, sustainable investing could represent between 30% and 35% percent of global assets under management. These ratios should be considered with great caution in so far as figures relate to different realities according to the asset managers and the countries.

Indeed to practice « sustainable investing », investors can implement various strategies : 1. Negative / exclusionary screening, 2. Positive/best-in-class screening, 3. Norms-based screening, 4. ESG integration, 5. Sustainability themed investing, 6. Impact/community investing, and 7. Corporate engagement and shareholder action. [6]

In fact the last three strategies (5,6,7) are largely related to combating climate change or addressing environmental or social challenges in line with the UN Sustainable Development Goals. According to the GSIA review, these investors’ priorities were in evidence throughout the five regions.

Culture does fit into the sustainability picture

If we consider the conclusion of the 1987 Brundtland Report we cannot ignore the fundamental role culture can play to promote harmony between human beings or to fuel the UN 2030 Agenda five P : planet, people, prosperity, peace and partnership. As soon as 1982, UNESCO in its Mexico City Declaration defined culture as « the whole complex distinctive spiritual, ritual, material, intellectual and emotional features that characterize a society or social group. It includes not only the arts and letters, but also modes of life, the fundamental rights of the human being, value systems, traditions and beliefs ». It claimed : « Culture is the essential condition for genuine development ». The cultural impulse is both individualistic (encouraging self-esteem) and collective (promoting social cohesion), which illustrates the huge scope of culture’s benefit to build and strengthen peaceful, creative and inclusive societies. The 2005 UNESCO Convention on the Protection and Promotion of the Diversity of Cultural Expressions states that cultural diversity « is a mainspring for sustainable development for communities, peoples and nations ».

Considering this high ambition displayed through these international instruments, cultural and creative industries (CCIs) which are part of the international community mentioned above, have a fundamental and specific social responsibility. By creating, producing and distributing content, they contribute to promote critical thinking, mutual understanding and people’s willingness to live together. CCIs and media companies including television, radio, newspapers, books, advertising, music, movie, performing arts, or video games have a responsibility for the impact their content has on people. It concerns what we listen, read or watch. The media exerts a strong influence on the decisions we make, the products we buy, the questions we ask to make our everyday lives .

The main stake here is not climate change or air pollution but cultural pluralism change or brains’ pollution.

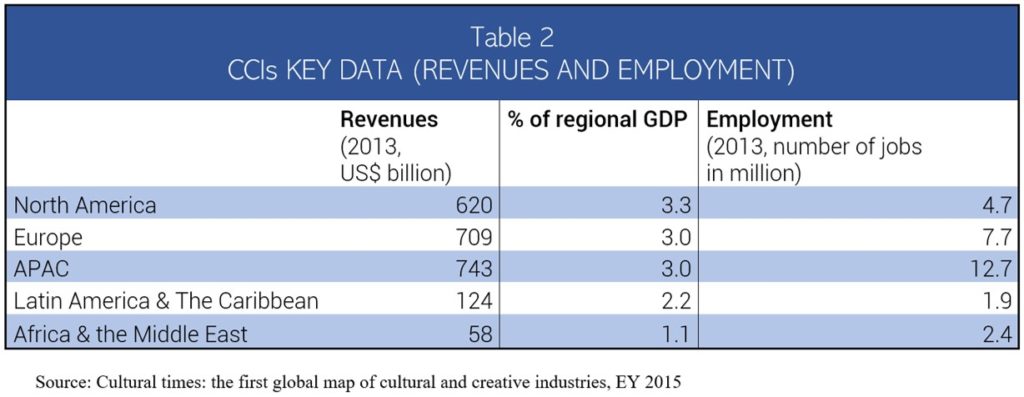

The CCIs and media sector is also powerful in terms of revenues and of employment (more than automative industry in Europe, the US and Japan combined). According to UNESCO, the CCIs are among the fastest growing sectors in the world. In 2013, they accounted for more than 3 % of the global economy : they generated annual revenues of US$ 2,250 billion and nearly 30 million jobs worldwide, employing more people aged 15 to 29 than any other sector. The same EY study specifies the CCIs sales worldwide exceed those of telecom services (US$ 1,770b globally) and surpass India’s GDP (US$ 1,900b).

The Arts and Cultural Production Satellite Account (ACPSA) released by the U.S. Department of Commerce Bureau of Economic Analysis (BEA) shows arts and cultural economic activity accounted for 4.3 percent of gross domestic product (GDP), or $804.2 billion in 2016. « Five million Americans are employed in arts and culture-related industries. The sector has expanded faster than the total economy every year since 2012, and its contribution to GDP is greater than agriculture or transportation. Economic growth in arts and culture is widespread across the nation. (Louisiana was the only state to see a decrease in 2016.) And the arts have consistently run a trade surplus for the U.S., delivering more cultural goods and services abroad than the nation imports. » Benjamin Wolff comments in Forbes, March 19, 2019.

Considering the contribution of the CCIs to economic growth and social cohesion, the poor appetite of investors for investing in culture can be surprising.

Yet culture is rarely on the sustainable investing menu…

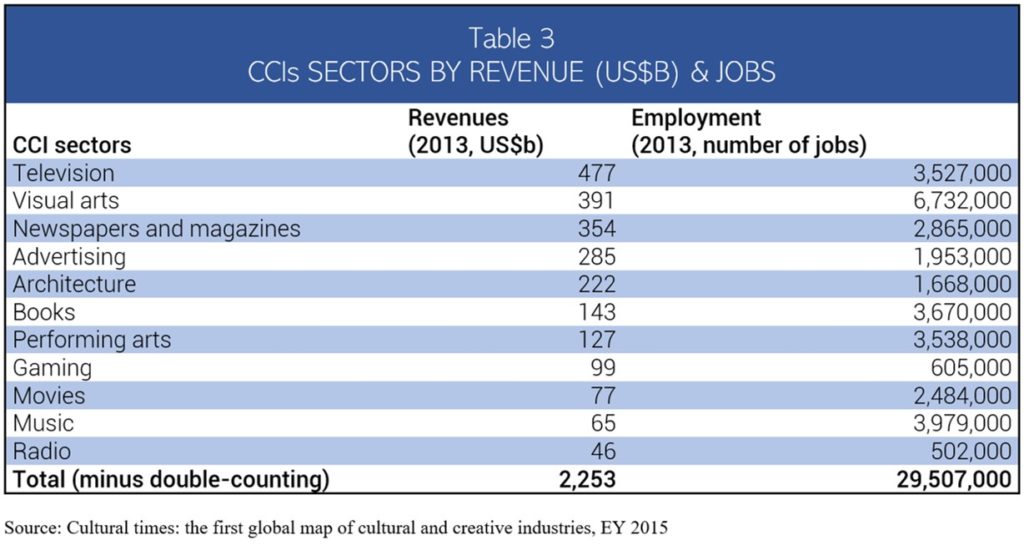

Among the reasons for the lack of interest of investors, that of the heterogeneity of the CCIs and media sector can be put forward (cf Table 3). The complexity of the business model is another : What is the sector’s value creation process ? How to assess governance ? What are the diverse products and services delivered? Who are the competitors ? Finally, the sector is often considered as an assisted activity dependent on public funding (taxes), the goodwill of individuals (crowdfunding) or company subsidies (charity). Cultural impact is neglected and often considered as a secondary impact in comparison with social and environmental impacts. This is a misguided analysis. The sector is an economic driver and fully contributes to strengthening the social fabric, the collective will and the self-esteem of individuals. At a time when the impact of investing is growing, as we have seen above, and mainly dedicated « to combating climate change or addressing environmental or social challenges in line with the UN Sustainable Development Goals », investors could further explore the potential of these arts and culture-related industries.

It can be recognized that the UN SDGs do not provide investors with much incentive to consider these issues as they do not directly target the sector. The recent European Council conclusions [7] on the Work Plan for Culture 2019-2022 recalled : « According to the ‘EU Charter of Fundamental Rights’ and the ‘UNESCO Convention on the Protection and Promotion of the Diversity of Cultural Expression’ artistic freedom is central to democratic societies. Art can help overcome barriers connected to race, religion, gender, age, nationality, culture and identity, by providing a counter-discourse and contesting privileged narratives and perspectives. » The EU Charter of Fundamental Rights recognizes in its article 11 that « The freedom and pluralism of the media shall be respected. » The UN Guiding Principles on Business and Human Rights themselves (Reporting framework wih implementation guidance-2015) include in « Relevant Human Rights » the following rights directly related to the CCIs and media sector, namely : rights to freedom of opinion and expression, rights to freedom of thought, conscience and religion, right to privacy.

It seems the UN SDGs do not have the same scope as regards « artistic freedom », or « freedom and pluralism of media ». UN SDG 4 Quality of education in its target 7 cautiously shelters « cultural diversity » under the umbrella of sustainable development’s concept [8]. That’s it. Brains reshaping which directly threats individuals’ critical thinking and the vitality of democracies is not really addressed by the UN SDGs which nevertheless define themselves as « the blueprint to achieve a better and more sustainable future for all. »

The largest market capitalizations such as Alphabet, Apple, Amazon, Facebook will be relieved, as massive and global content producers and distributors, to align with SDGs which do not challenge them on how they account for their material responsibility issues towards societies.

Nevertheless, a few investors are getting involved in this media and culture-oriented sector. The point here is not to deal with public financial institutions, banks or companies’ foundations, NGOs, who may propose loans or funds to this sector but to spot asset managers who claim culture as part of their investment portfolio.

This is the case for Triodos Bank N.V., a bank based in the Netherlands with branches in Belgium, Germany, United Kingdom and Spain. Triodos defines itself as « one of the world’s leading sustainable banks». With €15 billion as total assets under management, Triodos remains very far from Blackrock, the largest asset manager in the world with US$5.98 trillion in assets under management as of December 2018. But Triodos is paving the way when claiming : « Our mission is to make money work for positive social, environmental and cultural change » and stating that :« Arts and culture play an important role in the personal development of individuals and the cohesion of society as a whole. Creative expression provides new perspectives, inspires and connects people. » Apart from the declarations, in its annual report [9], Triodos details the outcomes of these investments in arts and culture-oriented companies : « Triodos Bank and Triodos Investment Management finance helped approximately 3,300 artists and creative companies active in the cultural sector (2017: 3,400). Theatre, music and dance productions from creative companies were attended by 1.2 million people. New productions in 2018 from the film and media sector financed by Triodos Bank (most importantly in Spain) were seen by approximately 13 million people (2017: 9 million). » Except for Triodos and a couple of others, the CCIs and media sector is the investor industry’s blind spot although it gives rise to both cultural, social and economic value.

This paper’s purpose is to highlight the necessity for investors to stress the urgency of investing not only money but also curiosity, time, energy, engagement in this sector with its specificities, its business risks and opportunities that deserve to be considered through their proper sustainability lens.

Large or emerging investment funds involved in the media and cultural sector, can (or cannot) locally and globally build remarkable bridges between human beings, stimulate individuals’ open minds and contribute to the people’s well-being. Because culture « makes a positive contribution to society », it deserves the full attention of the international community as a whole (governments, companies, opinion makers, think tanks, NGOs) should this community is sincerely determined to buil a sustained, peaceful and creative harmony among human beings. This is an imperative challenge to address the fears of populations fragilized by an accelerated process of globalization and uncontrolled migrations.

Pascale Thumerelle

Founder of Respethica

Paris, April 15, 2019

* Paper commissioned by the Dialogue of Civilizations Research Institute gGmbH

Notes :

1. Jean Tirole, Economie du Bien commun, PUF, 2016, p. 238 « Une entreprise compte en effet beaucoup de parties prenantes, c’est-à-dire d’acteurs affectés par les décisions de l’entreprise : les apporteurs de capitaux bien sûr, mais aussi les salariés, les sous-traitants, les clients, les collectivités territoriales où elle est implantée, les riverains qui pourraient subir des pollutions de sa part. »

2. https://sustainabledevelopment.un.org/sdgsummit

3. www.unpri.org/about-the-pri/about-the-pri/322.article

4. https://www.blackrock.com/corporate/investor-relations/2018-larry-fink-ceo-letter

5. http://www.gsi-alliance.org/wp-content/uploads/2019/03/GSIR_Review2018.3.28.pdf

6. Idem . The GSIA definitions of sustainable investment, published in the Global Sustainable Investment Review 2012, have emerged as a global standard of classification. These are: 1. NEGATIVE/EXCLUSIONARY SCREENING: the exclusion from a fund or portfolio of certain sectors, companies or practices based on specific ESG criteria; 2. POSITIVE/BEST-IN-CLASS SCREENING: investment in sectors, companies or projects selected for positive ESG performance relative to industry peers; 3. NORMS-BASED SCREENING: screening of investments against minimum standards of business practice based on international norms, such as those issued by the OECD, ILO, UN and UNICEF; 4. ESG INTEGRATION: the systematic and explicit inclusion by investment managers of environmental, social and governance factors into financial analysis; 5. SUSTAINABILITY THEMED INVESTING: investment in themes or assets specifically related to sustainability (for example clean energy, green technology or sustainable agriculture); 6. IMPACT/COMMUNITY INVESTING: targeted investments aimed at solving social or environmental problems, and including community investing, where capital is specifically directed to traditionally underserved individuals or communities, as well as financing that is provided to businesses with a clear social or environmental purpose; and 7. CORPORATE ENGAGEMENT AND SHAREHOLDER ACTION: the use of shareholder power to influence corporate behavior, including through direct corporate engagement (i.e., communicating with senior management and/or boards of companies), filing or co-filing shareholder proposals, and proxy voting that is guided by comprehensive ESG guidelines.

7. Official Journal of the European Union, 21.12.2018

8. SDG 4 « Target 4.7. By 2030, ensure that all learners acquire the knowledge and skills needed to promote sustainable development, including, among others, through education for sustainable development and sustainable lifestyles, human rights, gender equality, promotion of a culture of peace and nonviolence, global citizenship and appreciation of cultural diversity and of culture’s contribution to sustainable development »